In export and import, there are a variety of payment methods. You must hear about D/P and D/A and may be confused about what they are. Both the 2 payment terms belong to the documentary collection. Simply put, under D/P and D/A, buyers and sellers make transactions through banks, instead of direct transfer of money.

However, such simple knowledge is not enough if you tend to make international transactions by D/A or D/P. Today’s post is right for you and you can just navigate to related content via the following links.

What is D/A?

Under the payment term D/A, the abbreviation of Documents Against Acceptance, buyers can get shipping documents from the bank after the acceptance of a B/E, bill of exchange, and just make payments by the due date of the bill. For buyers, D/A is good as they can obtain the B/L to pick up goods before paying.

Take D/A 90 days for example. Notified by the bank, buyers will confirm the B/E and endorse “acceptance” on the bill, and then tell the bank “I will pay within 90 days. Believe me and give me shipping documents first.” The bank replies: “Okay, I trust you and release the documents for you to take delivery of goods.”

What is D/P?

Under D/P or Documents Against Payment, sellers instruct the bank to release documents only after buyers fully pay for the shipments.

Compared with D/A,

- The difference is that D/P terms require buyers to pay first and then get B/L to take over goods. From the seller’s standpoint, D/P is safer than D/A.

- The common point is that sellers surrender documents including the B/E and B/L and buyers make their payments through banks, instead of direct connections.

Typically, there are 2 common types:

- D/P at Sight, Documents Against Payment at Sight.

- D/P after Sight, Documents Against Payment After Sight.

D/P at Sight

Simply put, D/P at sight means that buyers pay for their order once they confirm there is no problem with documents like B/L.

Take 100% D/P at sight for example. The bank will notify the buyer to confirm documents and make a full payment to get them for the receipt of the goods. Usually, the buyer will go to the bank to pay or authorize the bank to directly deduct the amount from his account. After that, the buyer will get the B/L for customs clearance and cargo receiving.

D/P after Sight

Under D/P after sight, buyers are supposed to make a promise of the paid date with the bank. Before the promised payment date, the bank will keep B/E and shipping documents unreleased.

Generally, there are 3 ways to regulate the payment date under D/P after sight.

- xxx days payment after seeing the B/E.

- xxx days payment after the B/L date.

- xxx days payment after the date of issuance.

Additionally, some countries regulate xxx days payment after the arrival of the goods.

Concerning the payment term, it is often to see D/P 30-60 days after sight. Such payment terms are often used in long-distance ocean shipping. It might take 30 days or more to transport goods. Buyers can wait until goods arrive or approach the destination port, then finish all the payments to get the B/L. In this case, it can ease buyers’ cash flow pressures.

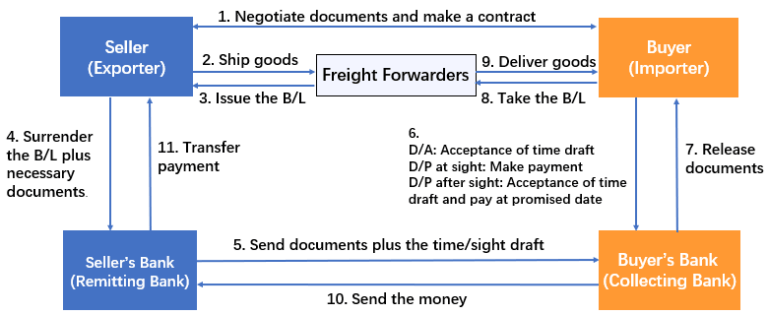

D/A and D/P Process Flow in 5 Steps (Example).

Actually, the process flow of D/A and D/P is roughly the same as the L/C’s, but there is no bank for credit guarantee.

Here I use an example to explain how D/P works in actual business.

Big retailer A, doing business in the USA, now imports a large number of daily products from China and asks for the D/P at sight to pay.

Step 1

After confirming with the Chinese supplier about the payment term D/P at sight, retailer A continues to communicate about what documents should be provided to the bank. As agreed, the B/L, commercial invoice, and packing list are necessary. More importantly, add relevant info to a contract and sign it.

Quick Note

In some cases, you might need the certificate of origin or other documents. So here the key is to communicate with your supplier in advance and make that clear.

Step 2

After the goods are shipped, the Chinese supplier will get the B/L from the freight forwarder and send it plus other necessary documents to the bank.

Step 3

The Chinese supplier’s bank will deliver the sight draft and documents to the buyer’s bank. Oftentimes, the supplier will clearly instruct the bank on how to send documents.

Step 4

Once receiving the documents, the bank will notify Retailer A to confirm the sight draft and will release documents only after retailer A has made the full payment.

Quick Note

Under D/P, generally, the buyer’s banks won’t release documents without receiving the money. Although some small banks might not behave like that, this possibility is very low. Because most banks are not willing to risk their credit on one client’s order. After all, bank credit is often higher than business credit.

If under D/P after sight, there exists an extra step — acceptance of the draft. Until the promised date, buyers have to finish all the payments. Then, the bank releases documents.

If under the D/A term, things are different — documents will be released after buyers sign and promise the paid date to the bank.

Step 5

After receiving the payment from Retailer A, the bank will send the money to the Chinese supplier’s bank, which will transfer it to the supplier.

D/P and D/A flow-process diagram

Key Info You Must Know When Using D/P and D/A.

Either under D/P or D/A payment terms, banks won’t provide the credit guarantee, or review the contents of documents. So, DP and DA are essentially a kind of trade financing on the basis of business credit.

Many importers are willing to use D/P and D/A. While for sellers, both are risky, as they have to undertake a big loss once the importer refuses to pay. So sellers take into account the importer’s credits and ability to pay.

In practice, D/P and D/A terms are often limited to old clients with a good reputation and long-term cooperative relationships. If you first place an order with a Chinese supplier and ask for D/P and D/A payment, the supplier would investigate your business credit and operations, as well as your bank’s reputation and rank, then evaluate whether it is safe or not.

If using DP or DA, suppliers usually take the following actions to reduce risks.

- Choose to quote a CIF price, in order to reduce the loss if goods are damaged or lost during transit and the buyer refuses to pay.

- Ask for a deposit, usually 30%-50% prepayment of the order value.

- Use “To Order” BL, instead of Straight B/L. If the buyer’s capital chain is broken due to local market factors and fails to pay, the goods would be held at the destination port and be auctioned once exceeding the storage period. At the auction, the consignee (buyer) on Straight B/L has a right of first refusal.

- Add export credit insurance for another layer of protection. In the event that the buyer goes bankrupt after goods are delivered, suppliers can find insurance firms for compensation.

Once more thing, under DP/DA, sellers might level up the quoted price as they have to prepay for material purchase, production, etc. So it’s not wise for buyers to go crazy about D/P or D/A payment terms.

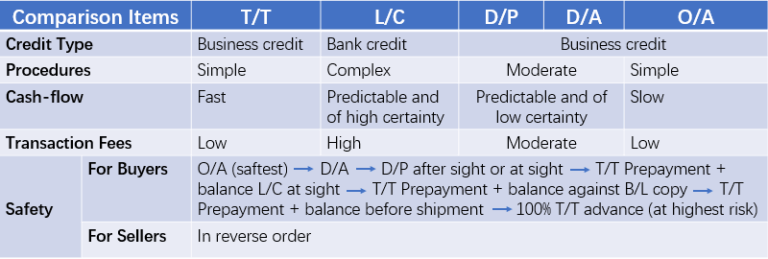

Among D/P, D/A, L/C, T/T, and O/A, which payment method is better?

In global trading, there are 5 most common payment methods: T/T, L/C, D/A, D/P, and O/A. I believe you must have a good understanding of DP and DA when reading here. Next, I’ll briefly introduce the remaining 3 payment methods, focusing on the comparison with DP and DA. So you’ll know which method is suitable for you.

T/T (Telegraphic Transfer)

T/T is also called wire transfer. Simply put, it is a money transfer, whereby buyers send the money to the foreign exchange bank designated by sellers. One of its advantages is the low bank transaction fees, usually $20 to $80. For specific transaction charges, you’d better check that with your local bank.

T/T is a common way for small and medium buyers to make international transactions. According to the time of payments, there are basically 3 kinds of T/T.

- 100% T/T advance, i.e., 100% T/T prepayment before production. This is the safest method for sellers while it is a big risk for buyers. In practice, it is used for sample orders or small orders.

- 100% T/T against B/L copy. This is not safe for sellers, as T/T is essentially a payment built on business credit, which is the same as DP and DA.

- T/T deposit + T/T balance before shipment or T/T balance against B/L copy. The deposit is generally 10%-50% of the order value. The most common is 30%.

If you place a large order (e.g. $ 1 million), it is not suitable to use “30% T/T prepayment + 70% T/T balance before shipment”. For you, it is a risk to pay $300,000 in advance. But if the deposit is too small, the supplier will feel insecure. In this case, a common practice is to make the “split payment”. Specifically, after signing a contract, you can make,

- 3% payment for the purchase of raw materials

- 7% payment after the material inspection

- 10% payment after producing 30% of products

- 10% payment after producing 60% of products

- 30% payment after full production and quality inspection

- Balance (40%) against the B/L copy

But the more times you transfer money, the higher the total transaction fees. Actually, L/C is the most common payment method for large business deals.

L/C (Letter of Credit)

In international trading, the L/C payment term is very secure, as third-party banks offer guarantees. The bank credit is higher than business credit.

And L/C can help you with the pressure on cash flow, as you don’t need to pay the supplier in advance. Your bank ensures the supplier will receive the payment once the cargo is shipped or arrives at the port of destination.

Typically, L/C is suitable for you in the following situations,

- Large order transactions.

- Not familiar with the supplier.

- There exists foreign exchange control, such as in Morocco.

Please note that under L/C, the requirements for documents are strict and transaction fees charged by banks are high. Therefore, L/C is not suitable for small orders.

O/A (Open Account)

O/A is a type of credit loan method to pay. After the goods are shipped, sellers directly send the B/L and other essential documents to buyers, then wait for the promised paid date to receive payments.

As you can see, order payments are completely built on the buyer’s credit, just like D/A. For buyers, this is the safest. In real business, big buyers often pay for orders in this way, for example, O/A 60 days.

While for sellers, O/A is highly risky, only limited to old clients with very high business credit. Oftentimes, sellers would ask for more conditions and protections for extra credit insurance.

Infographic on Cmparison of D/P, D/A, L/C, T/T, and O/A.

Considering different factors, each payment method has advantages and disadvantages. To be honest, there are no best international payment methods. You can choose a suitable one and negotiate with your supplier.

JingSourcing provides good, flexible payment terms to help you de-stress about cash flow and grow your business.

The End

Reading here, I believe you’ll get a deeper understanding and know how to use D/A and D/P. If you think this article is helpful, please leave your comment and share it.

We’re Jingsourcing, a leading sourcing agent in China. Based on years of experience, we provide high-quality and flexible services, including but not limited to product sourcing, quality inspection, shipping, private label, Amazon FBA solutions, etc. Feel free to contact us if you need any support when importing from China.